An ERISA bond holds administrators accountable to the law, ensuring they uphold ethical standards and fulfill their fiduciary role when handling employee retirement plans. Our guide covers everything you need to know about ERISA bonds, from how they work to who needs one, specific requirements, how much they cost, and more.

What is ERISA?

ERISA stands for Employment Retirement Income Security Act, a federal law enacted in 1974 to regulate retirement and health plans in private industry. Its regulations apply to most retirement plans, excluding the following:

- Those maintained or established by governmental entities or churches for their employees

- Offshore plans (those held outside of the United States)

- Other specialized plans

ERISA was enacted to provide more transparency and protection for employee retirement funds. It established requirements that plans provide participants with detailed information to understand how their money is managed and how to obtain benefits. ERISA also requires that plans establish avenues for participants to pursue grievances for denial of benefits or suspected mishandling of funds.

That’s where ERISA bonds come in.

Get Your ERISA Bond:

What is an ERISA bond?

ERISA established fiduciary responsibilities for those who manage and control retirement plan assets. These are specific standards of conduct that require each individual (“fiduciary”) to act in the best interests of the plan (the “principal” or “beneficiary”) rather than their own interest. A fiduciary handles money or other assets (i.e., retirement funds) for others. According to the Department of Labor, “the primary responsibility of fiduciaries is to run the plan solely in the interest of participants and beneficiaries and for the exclusive purpose of providing benefits and paying plan expenses.”

A Surety Bond to Protect Retirement Funds

Because plan administrators have significant power over employees’ retirement funds, ERISA does not rely on good faith to ensure that fiduciaries fulfill these duties. Instead, it requires that plan administrators with fiduciary duties obtain surety bonds.

How do ERISA fidelity bonds work?

Like other surety bonds, ERISA bonds are three-party agreements between a surety, an obligee, and a principal.

- Surety: The financial institution that issues the bond

- Obligee: The plan and its beneficiaries that may benefit from the bond if the principal breaks the bond contract

- Principal: The fiduciary (administrator) who must purchase the bond

What ERISA Bonds Cover

If an administrator commits misconduct like fraud or embezzlement or otherwise intentionally breaches their duty in a way that financially damages the plan, a type of surety bond called an ERISA fidelity bond protects the plan from loss. These fidelity bonds are essentially a form of insurance against wrongful or illegal acts by a plan’s fiduciaries. However, unlike fiduciary liability insurance, ERISA fidelity bonds operate to replace funds stolen from a company’s employee benefit plan. Such bonds do not insure anyone against any civil or criminal liabilities. The coverage these bonds provide is entirely distinct from that of fiduciary liability insurance, which can protect a plan and its fiduciaries against losses caused by unintentional mismanagement.

How much does an ERISA bond cost?

Determining Your Bond Amount

Like other types of surety bonds, ERISA bonds cost a small percentage of the bonded amount. Typically, the bond amount is 10% of the funds an official handles, with a minimum of $1,000 and a maximum of $500,000 (or $1,000,000 for plans that include employer-sponsored securities like company stock or bonds).

This guideline applies to plans with mostly “qualifying” assets (funds in bank accounts, mutual funds, products, and insurance policies). For plans that hold more than 5% of their value in “non-qualifying assets” (e.g., real estate, fine art, collectibles, etc.), the bonds must be written for 10% of the total value of the plan’s assets or for the value of all non-qualifying assets – whichever is greater.

Calculating Bond Cost

Typically, the cost of the bond will be a small percentage of the bond amount. The cost of each bond is based on the applicant’s credit history and personal and business finances. The issuer of the bond – the surety – determines the cost by assessing the level of risk involved in the bonding. The surety considers factors like credit score, business documents, assets, and liquidity.

Bonds typically are more expensive for parties with less favorable credit.

Because ERISA fidelity bonds protect the plan and its assets, the plan is permitted (but not required) to pay for their cost.

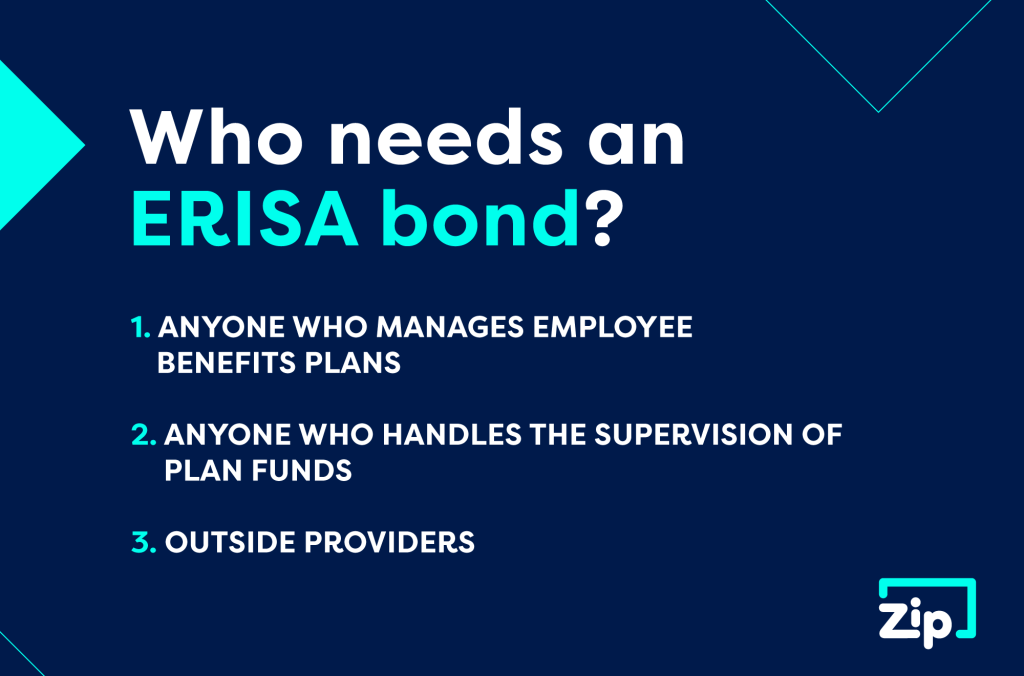

Who needs an ERISA fidelity bond?

1. Anyone Who Manages Employee Benefit Plans

Any individual who manages or handles funds, property, or other assets in employee benefit plans, including pensions, must obtain a first-party ERISA fidelity bond. A person fits this description if they fall into any of these categories:

- They have physical contact with checks, cash, or other similar property.

- They have physical contact with checks, cash, or other similar property.

- They can secure physical possession of plan funds.

- They have the potential ability to transfer plan funds to themselves or to third parties.

2. Anyone Who Handles the Supervision of Plan Funds

It also applies to individuals who supervise the handling of plan funds. Typically, this group includes:

- Plan trustees

- Plan sponsors

- Plan administrators

- Members of a plan’s investment committee

- Plan employees

- Plan sponsor employees

3. Outside Providers

Sometimes, plans will outsource some of their plan maintenance or investment functions. Some outside providers must be bonded under ERISA bond requirements, but others are exempt. The plan fiduciaries are responsible for accurately determining what bonding is necessary and ensuring that external service providers are properly bonded. Obtaining “third-party” ERISA bonds covering these contractors may be necessary.

People Also Ask

Do all fiduciaries need an ERISA bond?

No. Fiduciaries who do not handle funds are not required to obtain an ERISA fidelity bond.

What are my ERISA bond requirements?

ERISA fidelity bonds must meet the substantive requirements of ERISA section 412 and the appropriate regulations for the persons and plans involved. Only bonds obtained from a surety or reinsurer named on the Department of the Treasury’s Listing of Approved Sureties, Department Circular 570 (available on the Bureau of the Fiscal Service website), or in some cases from underwriters at Lloyds of London, are allowable under the law.

Neither the plan nor any interested party is permitted to have any control or significant financial interest (directly or indirectly) in any surety, reinsurer, agent, or broker through which the bond is obtained.

What type of bond form should I use?

Plans may meet their ERISA fidelity bond requirements using several different types of bond forms, including the following:

- Individual bonds

- Name schedule (covering the listed individuals)

- Position schedule (covering each of the job positions listed in the schedule)

- Blanket (covering all officers and employees of the insured generally)

Discussing your options with an experienced financial professional can help you reduce the cost of bonding while ensuring your plan protects its assets and meets its obligations.

How long does an ERISA bond last?

ERISA fidelity bonds can be written for a term of at least one year. Bonds that cover multiple years typically contain an “inflation guard” provision. Their coverage amounts automatically satisfy ERISA yearly, regardless of inflation and plan growth.

Get an ERISA Bond in Your State

ZipBonds offers ERISA bonds in all 50 states, and we’ve made the bonding process easier and faster than ever. Start your application online or over the phone by calling (888) 435-4191. One of our agents will happily help you complete the bonding process as quickly as possible.

About ZipBonds.com

Founders Ryan Swalve and Zach Mefferd formed the vision for ZipBonds.com when they realized how overly complicated it was to help clients place surety. The frustration of being unable to incorporate the technology they’d used in other insurance-focused projects left them thinking “there has to be a better way.”

Fast forward a couple of years, and that better way is the impetus of everything we do at ZipBonds. We constantly look for innovative ways to improve the bonding process for our clients and agents. Our team comprises individuals who understand all angles of surety – for companies, agencies, and individuals. Incorporating everyone’s point of view to improve the process while simultaneously integrating cutting-edge technology is what sets our business apart.